Complete Guide to Crypto Taxes for 2023: What Legal Businesses Need to Know

In the United States, digital payments and the associated cryptocurrency transactions have become increasingly popular in business activities. However, for companies registered as legal businesses, navigating the tax implications of handling digital payments can be a complex process. In this article, we will discuss whether legal businesses operating locally in the United States are required to pay taxes, the types of taxable service transactions involved, the forms and materials required, and the tax season and timeline each year.

Table Of Contents

1.Do Legal Businesses Need to Pay Taxes Locally in the USA?

In the United States, legal businesses, whether they are sole proprietorships, partnerships, or corporations, are required to pay taxes to the Internal Revenue Service (IRS) in accordance with tax laws. Whether you are involved in a traditional industry or the digital payments business, if your company operates in the United States, you are required to comply with tax regulations and pay taxes on time.

For digital payment businesses, which include accepting cryptocurrencies as payment or earning profits through cryptocurrency transactions, these activities also fall within the scope of tax reporting. According to the IRS, cryptocurrencies are considered property rather than legal tender, so their transactions and profits are subject to taxation, similar to other assets.

It is important to note that failure to report and pay taxes on income derived from digital payment activities can result in tax issues and penalties. Therefore, as a legal business, it is crucial to ensure compliance with tax regulations. Consulting a professional tax advisor or accountant is essential to understand the specific tax requirements and obligations applicable to your business. They can provide accurate guidance tailored to your specific business situation and ensure compliance with relevant tax regulations.

2.Types of Taxable Service Transactions

In the United States, certain types of cryptocurrency transactions are typically subject to taxation. Here are some examples of taxable cryptocurrency transactions:

Cryptocurrency Trading Profits: If you have realized trading profits through buying and selling cryptocurrencies, these profits are generally considered capital gains and may be subject to taxation. When you sell cryptocurrencies at a price higher than their purchase price, you may be required to pay capital gains tax on the profits realized.

Cryptocurrency Used for Purchasing Goods and Services: If you use cryptocurrencies to purchase goods or services, these transactions may also be subject to taxation. Similar to transactions conducted with legal tender, these transactions may be subject to sales tax or use tax.

Cryptocurrency Payments for Wages and Salaries: If you pay wages or salaries to employees using cryptocurrencies, these payments may also be subject to taxation. These payments need to be reported and taxed according to regular wage income tax regulations.

Certainly! While it’s important to note that tax laws can vary and individual circumstances may impact tax obligations, here are a few scenarios in the United States where cryptocurrencies may not be subject to taxation:

Personal Use Exemption: If you use cryptocurrencies solely for personal transactions, such as purchasing goods or services for personal use, there may be cases where the transaction falls below the threshold for tax reporting. However, it’s important to keep in mind that if you’re using cryptocurrencies for business purposes or investment, different tax rules may apply.

Gifts and Donations: If you receive cryptocurrencies as a gift or make a charitable donation using cryptocurrencies, there may be circumstances where you won’t be immediately taxed on the value of the gift or donation. However, if the gift or donation exceeds a certain value, there may be reporting requirements or potential tax implications.

Like-kind Exchanges (1031 Exchanges): In the past, there was some debate around whether cryptocurrency-to-cryptocurrency exchanges qualified for like-kind exchanges under Section 1031 of the Internal Revenue Code. However, as of tax year 2018, the Tax Cuts and Jobs Act limited like-kind exchanges to real property only, eliminating this option for cryptocurrencies.

Losses and Capital Loss Deductions: If you experience losses from the sale or exchange of cryptocurrencies, you may be able to offset your capital gains taxes by deducting those losses. Capital losses can be used to reduce your overall taxable income, potentially resulting in a lower tax liability.

3.Forms and Materials Required

Here is a brief overview of the general forms and materials required for digital payment-related tax reporting in the United States, along with simplified step-by-step instructions:

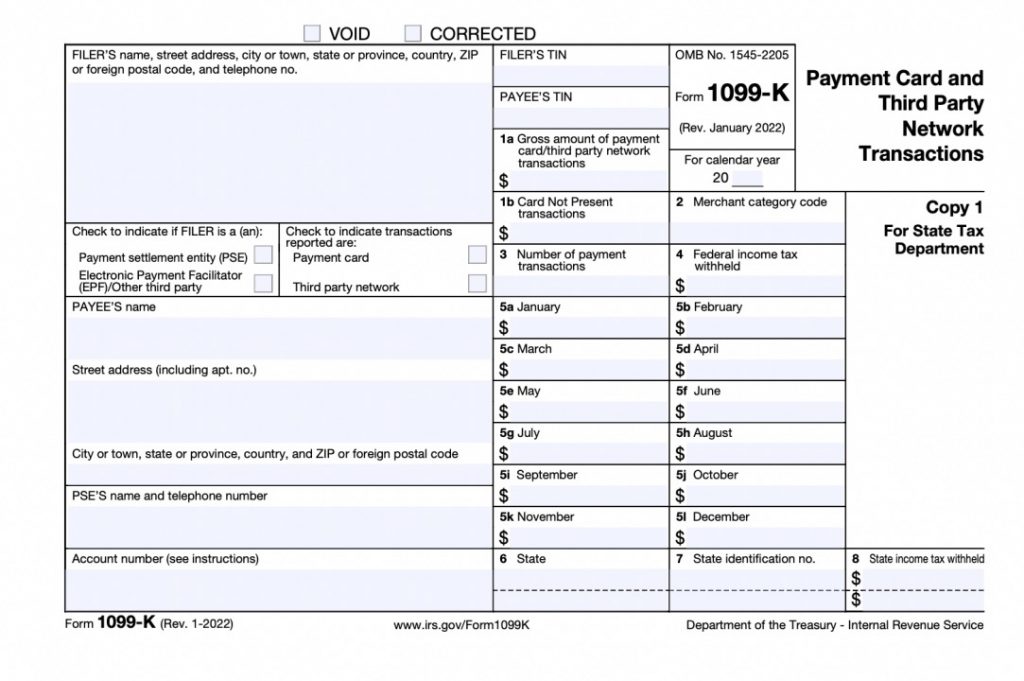

Form 1099-K: This form is used to report the total cryptocurrency transaction amounts obtained through payment processors. You may need to obtain this form from exchanges or payment processors and use the relevant data in your tax filing.

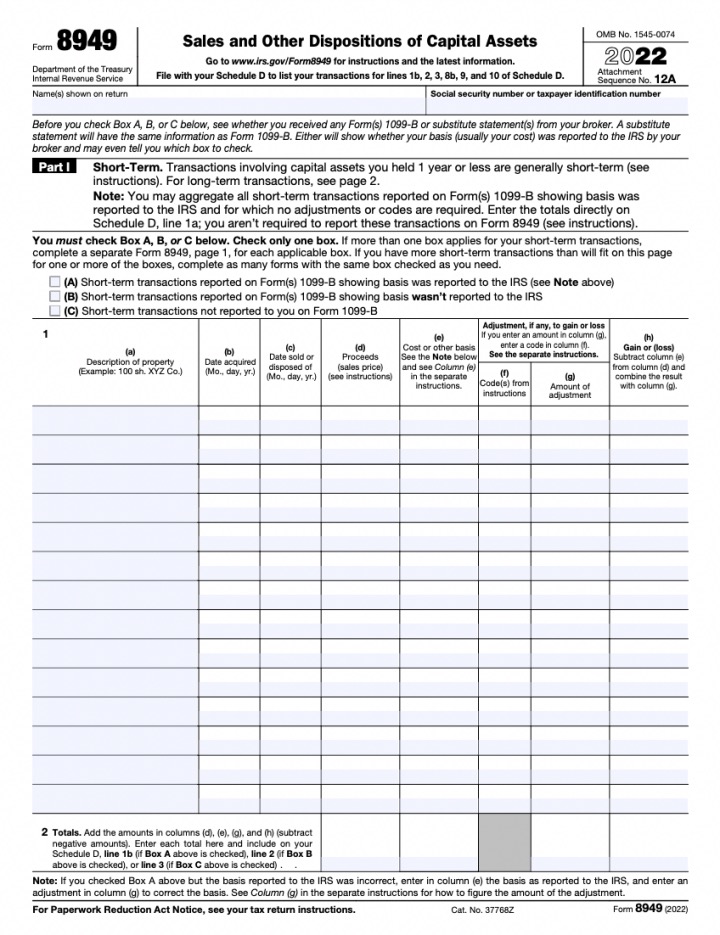

Form 8949:

This form is used to report the buying and selling of cryptocurrencies and investment transactions. You need to provide information such as the purchase price, sale price, and relevant dates for each transaction, following the instructions on the form.

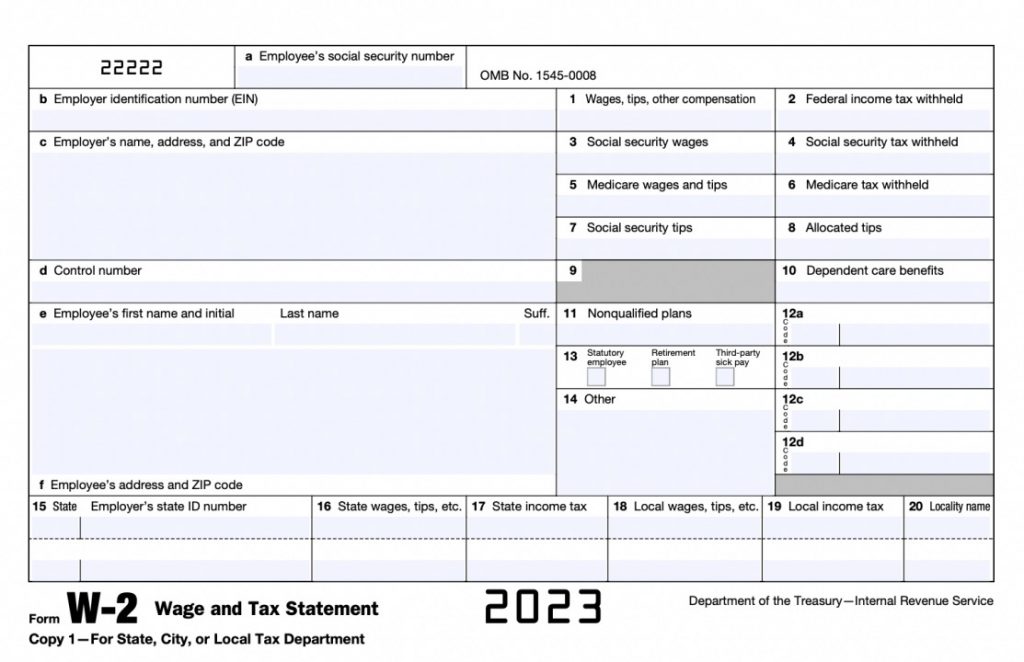

Form W-2:

If you use cryptocurrencies as a payment method for wages and salaries, you may need to use the W-2 form to report these payments. This form is used to report employees’ wage income and usually requires detailed wage payment records.

In addition to forms, here are some common materials that may need to be provided during the tax filing process:

Transaction records: This includes all transaction records related to digital payments, such as buying and selling transactions, investment transactions, and transactions where cryptocurrencies were used to purchase goods or services. Ensure that the records are clear, complete, and organized in chronological order.

Recording Wallet Addresses: If you conduct transactions using multiple cryptocurrency wallets, it is crucial to record the addresses and relevant information for each wallet. This record will be useful when required to provide details in the future.

Income and Expenditure Records: Maintain comprehensive records of all income and expenses related to digital payment activities, including transaction fees, service charges, and other business-related costs.

Bank and Exchange Statements: If you have accounts with banks or cryptocurrency exchanges, it may be necessary to obtain corresponding reports and account summaries to reference during tax filing.

Step-by-step Instructions:

- Collect all transaction records, wallet address records, and income and expenditure records associated with digital payment activities.

- Ensure you have obtained the necessary forms (such as 1099-K, 8949, and W-2) or request them from the relevant institutions.

- Fill out the forms and provide the required information following the instructions provided. Make sure to accurately record the buying and selling prices, dates, and relevant details for each transaction.

- Submit the forms and relevant materials along with your tax return to the Internal Revenue Service (IRS) during tax filing.

4.Tax Season and Timeline:

January:

- Collect and organize the previous year’s digital payment transaction records and materials.

- Prepare the required forms and documents.

February:

- Continue preparing tax forms and documents.

- Ensure you have obtained all necessary forms and materials.

March:

- Complete the preparation of tax forms and documents.

- Submit the tax return and make the tax payment.

April:

- The tax season deadline typically falls in mid-April, but the specific date may vary depending on the year and holidays.

- Ensure that the filing and payment are completed before the deadline.

Note: The deadline may be subject to adjustments due to special circumstances, so it is advisable to stay updated with official announcements and updates from the IRS. Additionally, certain conditions may allow for filing extensions. For example, if you are a sole proprietor, you can apply for a personal income tax extension until October.

No Comments