Tokenized Treasuries Take Over: How RWAs Became On-Chain Collateral in 2026

As of January 2026, the financial landscape has been irrevocably altered by the maturation of the Real-World Asset (RWA) sector. What began in the early 2020s as a speculative narrative regarding the “tokenization of everything” has solidified into the dominant structural theme of the 2025-2026 market cycle. We are no longer discussing pilot programs or proofs of concept; we are witnessing the industrial-scale migration of traditional financial instruments onto distributed ledger technology. The “Great Convergence” of Traditional Finance (TradFi) and Decentralized Finance (DeFi) is not a future event—it is the current operating reality.

The catalyst for this seismic shift was the passage of the Guiding and Establishing National Innovation for U.S. Stablecoins Act (GENIUS Act) in July 2025. This landmark legislation provided the regulatory clarity required for the world’s largest asset managers to enter the arena with conviction. Consequently, 2025 saw the RWA market explode in complexity and valuation. Tokenized U.S. Treasuries have surged to a market capitalization between $7 billion and $9 billion, growing approximately 50-fold since early 2024.Real estate tokenization has moved beyond novelty to facilitate institutional-grade settlement, and private equity giants like Hamilton Lane and KKR have normalized the distribution of alternative assets via blockchain rails.

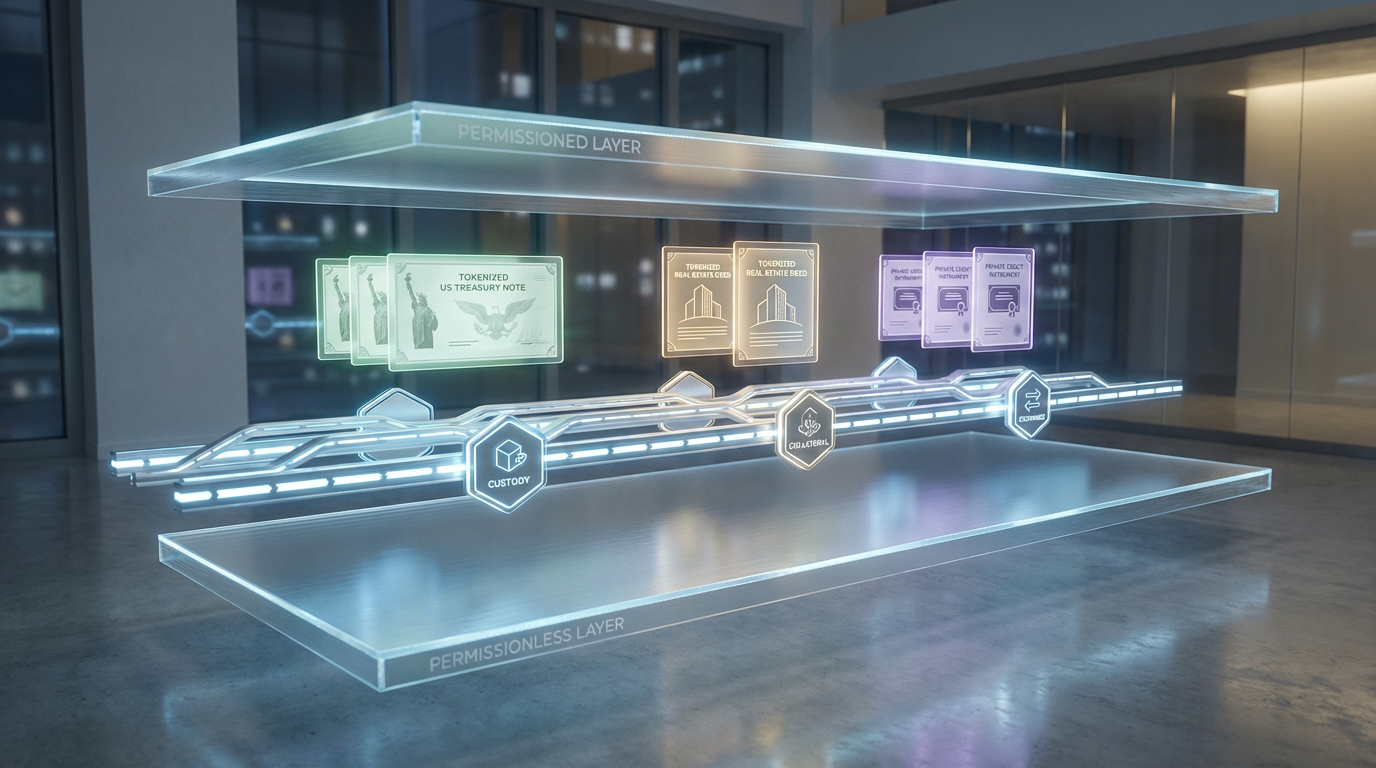

The market structure has bifurcated into two distinct but symbiotic layers: a regulated, “permissioned” layer dominated by giants like BlackRock and Franklin Templeton, and a permissionless DeFi layer that wraps and utilizes these assets as pristine collateral. The tension and integration between these layers define the current opportunity set. BlackRock’s BUIDL fund, having distributed over $100 million in cumulative dividends by late 2025, serves as the flagship for institutional adoption.However, the dynamic nature of the crypto-native economy was highlighted in January 2026 when Circle’s USYC fund flipped BUIDL in Total Value Locked (TVL), driven by superior integration into DeFi collateral flows.

This report offers an exhaustive analysis of the RWA sector as of January 2026. It dissects the regulatory frameworks, asset class performance, infrastructure battles, and strategic implications for investors. It concludes with a high-conviction perspective from our lead analyst, Ricky, and offers granular projections through 2030.

1. The Macro-Structural Shift: 2025 in Review

To understand the current dominance of the RWA narrative, one must analyze the macroeconomic and regulatory pressures that forged the market of 2026. The years 2024 and 2025 were characterized by a “flight to quality” within the digital asset ecosystem, driven by high nominal interest rates and the exhaustion of purely speculative crypto cycles.

1.1 The End of Zero-Interest Rate Policy (ZIRP) & The Yield Hunger

The defining economic feature of the 2025-2026 cycle remains the persistence of positive real interest rates. With the Federal Reserve maintaining rates to manage the “last mile” of inflation stabilization, the opportunity cost of holding non-yielding assets became untenable for both retail and institutional capital.

In previous crypto cycles (2020-2021), the “risk-free” rate was near zero, incentivizing capital to seek yield in highly speculative DeFi protocols or unbacked algorithmic stablecoins. By 2025, the risk-free rate provided by U.S. Treasury bills hovered between 4% and 5%. This created a massive hydraulic pressure to bridge these “real-world” yields onto the blockchain. Investors refused to leave billions of dollars in non-interest-bearing stablecoins (like standard USDT or USDC) when they could hold tokenized Treasury products that offered government-backed yield with similar liquidity profiles. This arbitrage—between on-chain sterility and off-chain yield—was the primary engine of RWA growth.

1.2 The “Institutional Production” Phase

The experimental phase of 2023-2024 definitively ended in 2025. Major financial institutions transitioned from “innovation lab” pilots to core business integration.

- BlackRock: Through its partnership with Securitize, BlackRock did not just launch a product; it integrated BUIDL into the collateral fabrics of major exchanges like Binance and Deribit, effectively turning T-bills into a margin asset for crypto trading.

- State Street & BNY Mellon: These custodial giants aggressively moved into the back-office administration of tokenized assets, recognizing that the “ledger of record” for financial assets is shifting from centralized SQL databases to distributed networks.

- Goldman Sachs & BNP Paribas: Through the Canton Network, over 30 institutions began piloting tokenized bonds and gold, validating the thesis that blockchain is the future settlement rail for wholesale finance.

This institutional entry was not merely about creating new products; it was about collateral efficiency. In a high-rate environment, capital efficiency is paramount. The ability to post tokenized assets as collateral 24/7 without T+2 settlement delays unlocked billions in capital efficiency, driving the adoption of RWA not just as an investment, but as a utility.

2. The Regulatory Watershed: The GENIUS Act of 2025

The single most consequential event shaping the 2026 landscape was the enactment of the Guiding and Establishing National Innovation for U.S. Stablecoins Act (GENIUS Act). Signed into law by President Donald Trump on July 18, 2025, this legislation effectively merged the digital asset economy with the U.S. dollar hegemony.

2.1 Anatomy of the Legislation

The GENIUS Act was drafted with a clear geopolitical objective: to solidify the U.S. dollar as the settlement layer of the internet and counter the rise of foreign digital currencies. It established the first comprehensive federal framework for digital assets in the United States, replacing the patchwork of state-level money transmitter licenses that had previously governed the sector.

Key Provisions and Market Impact:

- Strict Definition of Payment Stablecoins: The Act introduced a rigorous definition of “Payment Stablecoins,” restricting issuance to three categories of highly regulated entities: subsidiaries of insured depository institutions (banks), OCC-chartered non-bank entities, and state-qualified issuers (subject to a $10 billion cap before federal oversight kicks in).

- The 1:1 Reserve Mandate: Issuers are now legally required to maintain reserves on a strictly 1:1 basis. These reserves must be comprised solely of cash, U.S. Treasury bills (with a maturity of less than 93 days), and repurchase agreements backed by Treasuries.This provision effectively eliminated the commercial paper and corporate debt backing that characterized early stablecoin iterations, forcing stablecoin issuers to become some of the largest buyers of U.S. government debt in the world.

- The Ban on Algorithmic Stablecoins: In a direct response to the Terra/Luna collapse of the previous cycle, the Act explicitly excluded algorithmic stablecoins or those not fully backed by qualifying assets from the definition of payment stablecoins.While not strictly illegal to code, these assets are effectively barred from the U.S. banking system and cannot be marketed as “stablecoins.”

- Segregation of Funds: The Act mandates the complete segregation of customer funds (reserves) from the issuer’s corporate funds, ensuring that in the event of an issuer’s bankruptcy, token holders have a priority claim on the reserve assets.

2.2 The “No-Yield” Clause and the Rise of Investment Tokens

Crucially, the GENIUS Act prohibits “Payment Stablecoins” from paying interest or yield directly to holders.This provision was included to protect commercial banks from deposit flight; if a stablecoin functioned exactly like a high-yield savings account but with instant transferability, banks feared a massive exodus of deposits.

However, this regulatory firewall unintentionally catalyzed the explosion of the Tokenized Treasury market. Since users could not earn yield on their transactional dollars (USDC, USDT), capital fled into “Investment Tokens” like BlackRock’s BUIDL, Ondo’s USDY, and Franklin Templeton’s BENJI. These instruments are structured as securities rather than payment tokens, allowing them to legally pass the yield of the underlying Treasuries to the holder. The GENIUS Act, therefore, created a bifurcated market: Payment Tokens for velocity and settlement, and Investment Tokens for savings and collateral.

3. Tokenized Treasuries: The Bedrock of On-Chain Finance

If stablecoins are the checking accounts of the crypto economy, Tokenized Treasuries have become its savings accounts—and increasingly, its prime collateral. This sector has witnessed explosive growth, surging 50x from early 2024 to reach a market cap between $7 billion and $9 billion by January 2026.

3.1 The Battle of Giants: BlackRock vs. Circle

For much of 2025, BlackRock’s USD Institutional Digital Liquidity Fund (BUIDL) was the undisputed leader of the sector, peaking at over $2 billion in assets under management (AUM). However, the dynamics of the crypto-native economy spurred a shift in leadership in early 2026.

Launched in March 2024 on Ethereum, BUIDL was the first major product to offer institutional-grade, on-chain exposure to U.S. Treasuries.

- Performance: By December 2025, the fund had distributed over $100 million in cumulative dividends to investors.

- Structure: It operates as a “distributing” token, paying out monthly dividends in the form of additional tokens or stablecoins. This mimics traditional bond coupon payments.

- Integration: BUIDL achieved significant milestones in 2025 by becoming accepted collateral on major derivatives exchanges like Deribit and Binance.It also serves as the reserve backing for Ethena’s USDtb stablecoin, creating a deep integration with DeFi liquidity.

- Limitation: BUIDL is restricted to “Qualified Purchasers” (generally individuals with >$5 million in investments), limiting its direct user base to high-net-worth individuals and institutions.

In a watershed moment for DeFi mechanics, Circle’s USYC (a tokenized treasury product) flipped BUIDL in January 2026, reaching $1.69 billion AUM compared to BUIDL’s $1.68 billion.

- The “Accumulating” Advantage: Unlike BUIDL, USYC is an “accumulating” token. The yield is reflected in the increasing Net Asset Value (NAV) of the token itself rather than through taxable dividend distributions. This structure is highly preferred in DeFi, as it simplifies tax reporting and increases the capital efficiency of the token when used as collateral.

- Access: USYC targeted a broader institutional base with lower minimums ($100k) and aggressive integration into non-US markets, capturing the “mid-market” flow that BUIDL’s high entry barriers excluded.

3.2 The Mid-Market and Retail Bridges: Ondo and Franklin Templeton

While BlackRock and Circle battle for institutional dominance, other players have carved out significant niches.

- Ondo Finance (OUSG/USDY): Ondo has positioned itself as the bridge for the retail and semi-institutional market. Its USDY token functions as a yield-bearing note backed by U.S. Treasuries but is structured to be accessible to non-US retail investors, bypassing the strict Accredited Investor rules that gatekeep BUIDL. Ondo’s aggressive expansion onto high-throughput chains like Aptos, Sui, and Solana has made it the default “savings account” for the retail DeFi user.

- Franklin Templeton (BENJI): The Franklin OnChain U.S. Government Money Fund (FOBXX), represented by the BENJI token, remains a stalwart with approximately $892 million in AUM. BENJI is unique in its use of public blockchains (Stellar and Polygon) as the official record of ownership. However, its strict adherence to traditional transfer agency rules has made it less composable in DeFi compared to USYC or Ondo’s products.

3.3 The “Collateralization of Everything”

The most significant trend in 2026 is the use of these tokens as collateral. Traders are increasingly posting BUIDL or USYC instead of non-yielding USDT to margin their positions.

- Capital Efficiency: By posting yield-bearing assets as margin, traders offset their funding rates. If the cost to long Bitcoin is 10% annualized, but the collateral earns 5% risk-free, the effective cost of leverage is halved. This dynamic is driving the massive inflows into the sector.

- The “Russian Doll” Effect: Protocols like Ethena are creating stablecoins (USDtb) backed by BUIDL, which is backed by Treasuries. This layering increases system interconnectedness but creates robust, sticky demand for the underlying RWA tokens.

Table 3.1: Comparative Analysis of Top Tokenized Treasury Products (Jan 2026)

| Feature | BlackRock BUIDL | Circle USYC | Franklin Templeton BENJI | Ondo USDY |

|---|---|---|---|---|

| AUM (Jan 2026) | ~$1.68 Billion | ~$1.69 Billion | ~$892 Million | ~$1.3 Billion |

| Yield Mechanism | Distributing (Monthly) | Accumulating (NAV) | Distributing (Monthly) | Accumulating (Token Price) |

| Primary Chain | Ethereum | Ethereum / Multi-chain | Stellar / Polygon | Ethereum / Mantle / Sui / Aptos |

| Target Audience | Qualified Purchasers ($5M+) | Institutions ($100k+) | Institutional / Retail | Non-US Retail / Institutions |

| Collateral Use | High (Binance, Deribit) | Very High (DeFi Lending) | Low (Siloed) | High (DeFi Perps/Lending) |

| Regulatory Basis | SEC Reg D | SEC Reg D / Reg S | SEC Registered 1940 Act | Reg S (Offshore) |

4. Real Estate: From Fractionalization to Title Settlement

Real estate tokenization, a sector often criticized for high promises and low delivery, found its footing in 2025. The market has matured into two distinct verticals: Fractional Investment, which treats property as a financial asset to be sliced and traded, and Title Settlement, which uses blockchain to streamline the conveyance of physical deeds.

4.1 Title Settlement: The Propy Revolution

While fractionalization appeals to investors, Propy has focused on the infrastructure of home buying, achieving significant milestones in 2025.

- Infrastructure Expansion: In late 2025, Propy announced a $100 million expansion plan to acquire traditional title companies across key U.S. states like California, Florida, and Texas. This move represents a “roll-up” strategy, acquiring legacy businesses and migrating their operations to blockchain rails.

- Agent Avery: Propy launched “Agent Avery,” an AI-driven escrow officer. By combining AI processing with blockchain immutability, the platform has reduced closing times from the industry standard of 30 days to nearly instantaneous settlement for cash and crypto deals.

- On-Chain Deeds: Propy’s “Propy Map” now tracks live on-chain transfers in pilot markets like Arizona and Colorado, where state governments have begun to recognize blockchain records as valid parallel title systems.The issuance of the first BTC-backed real estate loan in January 2025 further demonstrated the bridging of crypto-wealth into hard assets.

4.2 Fractionalization: The “Stock Market” for Homes

Platforms like RealT, Lofty AI, and Binaryx have successfully tokenized hundreds of millions of dollars in residential property, creating a liquid market for an traditionally illiquid asset class.

- RealT (Ethereum/Gnosis): RealT continues to lead in volume, focusing on Section 8 and distressed housing in the US Rust Belt. Investors buy tokens representing LLC shares and receive daily rent payouts in stablecoins. By 2026, RealT has expanded into European properties and launched automated lending markets where users can borrow against their property tokens.

- Lofty AI (Algorand): Lofty has differentiated itself through its DAO governance model. Token holders for a specific property vote on operational decisions, such as rent increases, repairs, and eviction notices. This “governance-by-token” model has proven resilient, creating a highly engaged community of digital landlords. By mid-2025, Lofty had onboarded over 150 properties across 40 markets.

- Market Size: The fractional real estate market is estimated at approximately $20 billion in 2025, with aggressive projections suggesting it could reach trillions by the 2030s as regulatory frameworks in jurisdictions like Dubai (VARA) and the EU (MiCA) further accommodate these structures.

4.3 The Network City: CityDAO

CityDAO represents the experimental edge of real estate RWA. Owning land in Wyoming (Parcel 0) and governing it via a DAO structure, CityDAO is testing the limits of “Network Cities.” In 2025, the project expanded its mandate to explore the creation of special economic zones governed by on-chain charters. While still a niche sector compared to Propy or RealT, CityDAO highlights the potential for blockchain to reimagine municipal governance and zoning laws.

5. Private Credit & Debt Markets: The Yield Engine

While Treasuries offer safety, the “hunt for alpha” has driven capital into Tokenized Private Credit. This sector involves lending crypto-assets (usually stablecoins) to real-world borrowers, ranging from fintech startups in emerging markets to carbon credit originators.

5.1 The Renaissance of On-Chain Credit

Private credit protocols like Centrifuge, Maple Finance, and Goldfinch experienced a renaissance in 2025. After the credit contagions of 2022 (which were largely driven by uncollateralized lending to crypto trading firms), these protocols rebuilt with stricter underwriting standards and a focus on “real-world” productive assets.

- Centrifuge: Remains the infrastructure leader, facilitating loans for diverse asset classes including trade finance and structured credit. Their “legal wrapper” technology—connecting on-chain DAOs with off-chain Special Purpose Vehicles (SPVs)—has become the industry standard for ensuring legal enforceability of on-chain debts.

- Performance: Private credit yields in 2026 are tracking between 8% and 12%, significantly outperforming the 4-5% available in Treasuries. This spread has attracted DAO treasuries (like MakerDAO and Arbitrum) looking to diversify their idle stablecoin holdings into higher-yielding, off-chain debt.

- Market Dynamics: The total tokenized private credit market constitutes roughly 61% of the RWA sector (excluding stablecoins) as of mid-2025. This dominance highlights the demand for yield that exceeds the “risk-free” rate.

6. Private Equity: The Democratization of Access

2025 saw the breach of the “velvet rope” surrounding top-tier private equity. Firms like Hamilton Lane and KKR, in partnership with Securitize, have launched tokenized feeder funds that lower minimum investments from the traditional $5 million to as low as $10,000 or even $500 for certain retail-facing structures.

6.1 Institutional Feeder Funds

The mechanics of these funds involve a “Master-Feeder” structure where the tokenized fund (the feeder) aggregates capital from smaller investors and invests it into the main institutional fund (the master).

- Hamilton Lane: Has been the most aggressive traditional firm. By late 2025, they expanded their tokenized offerings to include infrastructure funds and private credit vehicles. Their partnership with Republic aims to bring these institutional-grade products to the mass affluent retail market.

- Liquidity Premiums: The primary value proposition here is not just access, but liquidity. Traditional PE funds lock capital for 7-10 years. Tokenized versions, trading on secondary markets (ATS) like Securitize Markets, offer the theoretical possibility of early exit, although liquidity in these secondary markets remains thin compared to public equities.

- New Inflows: Late 2025 saw significant inflows into Hamilton Lane’s tokenized funds, particularly their Private Infrastructure Fund (HLPIF) and SCOPE fund, driven by the launch on high-speed networks like Sei and Polygon which lowered transaction costs for retail participants.

7. Infrastructure: The Rails of the RWA Economy

The RWA boom has spurred a war for infrastructure dominance. General-purpose chains are competing with app-specific chains (AppChains) to host these high-value assets.

7.1 The Rise of MANTRA (OM)

One of the breakout stars of 2025 was MANTRA (OM). Positioning itself as a “Layer 1 for Security and RWAs,” Mantra surged to a market cap of nearly $7 billion by early 2026.

- The Thesis: General-purpose chains like Ethereum are too cluttered and expensive for regulated assets. RWAs require built-in compliance (KYC/AML) at the protocol level. Mantra provides this “walled garden” approach, appealing to institutions and regulators in jurisdictions like Dubai and Hong Kong.

- Ecosystem: Mantra has secured partnerships for tokenizing real estate in the UAE and is building a compliant DEX structure that prevents sanctioned wallets from interacting with pools.

7.2 Ethereum vs. The World

Despite the rise of specialized chains, Ethereum remains the “Main Street” of RWAs. BlackRock’s BUIDL and most major stablecoins live on Ethereum. The network effects of liquidity (where the buyers are) continue to outweigh the technical benefits of other chains. However, Solana and Sei are making aggressive inroads with high-throughput capabilities suited for high-frequency trading of tokenized assets. For example, Hamilton Lane’s launch on Sei demonstrated a demand for sub-second finality in financial transactions.

7.3 Oracles and Interoperability

As RWAs fragment across Ethereum, Avalanche, Base, and private bank chains, the ability to move value and data securely between them is paramount.

- Chainlink (CCIP): Has cemented its role as the “SWIFT of Blockchain.” Chainlink’s Cross-Chain Interoperability Protocol (CCIP) is now standard for moving tokenized assets between banking chains and public networks. Its Proof of Reserve (PoR) service is also critical for verifying the off-chain collateral of stablecoins and tokenized gold in real-time.

8. The Alpha View: A Perspective from Ricky

Note: The following section provides a direct, high-conviction market analysis from our lead crypto-asset strategist, Ricky. It adopts a more direct, trader-centric tone to cut through the corporate narrative.

“The Great Re-Hypothecation is Upon Us”

If you look beneath the hood of the 2026 crypto market, the story isn’t just about “adoption”—it’s about collateral efficiency. For the last decade, crypto was a closed loop. We printed magical internet money (tokens) to buy other magical internet money. When the cycle turned, the leverage unwound because there was no “real” value underpinning the system.

2026 is different. My perspective is simple: We are witnessing the financialization of the blockchain.

1. The Alpha is in the “Plumbing,” Not the Assets

Don’t just look at the tokenized assets themselves (the real estate tokens or the T-bills). Those are beta plays; they will track the S&P 500 or the Fed Funds Rate. The alpha is in the infrastructure that allows these cumbersome, regulated assets to move at the speed of crypto.

- Watch the Wrappers: Protocols that can legally wrap a restricted asset (like BUIDL) and make it usable in a permissionless lending protocol are the new “money printers.” They capture the spread between institutional access and retail demand. The flip of BUIDL by USYC wasn’t an accident; it was a victory for composability.

- Identity is the New Wallet: With the GENIUS Act enforcing strict KYC, “Identity Oracles” that prove you are a compliant citizen without revealing your data on-chain will be critical.

2. The “Fake” RWA Trap

Be wary of “RWA” projects that are just DAOs buying assets off-chain and putting a PDF receipt on-chain. That is not tokenization; that is a trust model with extra steps. The real innovation is happening where the legal settlement is atomic—where the token is the title (like Propy’s vision) or where the Regulation D offering is natively integrated into the code (like Securitize). If the token doesn’t represent legal claim in a court of law, it’s a memecoin with a tie on.

3. The Collateral Flip

The most bullish signal for the entire industry is that Bitcoin and ETH are no longer the only pristine collateral. When a trader can margin a position with a tokenized T-bill, the volatility of the entire crypto market dampens. We are importing stability. This means the “super-cycles” of 80% drawdowns might be over. It also means the insane 100x pumps might be rarer. The market is growing up.

4. The Geopolitical Play

Make no mistake: The GENIUS Act was a defensive move by the United States. By enforcing dollar-backing for stablecoins and banning algo-stables, the US has effectively turned every stablecoin user in Nigeria, Argentina, and Vietnam into a buyer of US debt. Crypto has become the distribution arm of the US Treasury. Betting against US-regulated stablecoins/RWAs is betting against the US government’s desire to fund its deficit. Never bet against the printer.

Final Thought:

We are in the “installation phase” of the RWA super-cycle. The infrastructure is built (Genius Act, BlackRock, Circle). The next 5 years (2026-2030) are the “deployment phase.” Expect friction, expect regulatory skirmishes, but the direction of travel is irreversible. Everything that can be tokenized, will be tokenized.

9. Future Projections: 2026-2030

Based on current adoption curves, the regulatory clarity provided by the GENIUS Act, and the institutional momentum observed in 2025, we project the following trajectory for the RWA sector through the end of the decade.

9.1 Market Sizing Scenarios

- Bear Case ($2 Trillion by 2030): In this scenario, strict regulation stifles innovation, restricting tokenization to inter-bank settlement layers. Retail participation remains blocked by “accredited investor” rules, and DeFi integration is outlawed.

- Base Case ($10 Trillion by 2030): (Aligned with Binaryx/21.co forecasts) Tokenized Treasuries become the standard for corporate treasury management. Significant portions of the real estate and private credit markets move on-chain. The “liquidity premium” of tokenization proves too valuable for issuers to ignore.

- Bull Case ($16+ Trillion by 2030): (Aligned with BCG/MANTRA projections) A full “repricing” of global assets onto blockchain rails occurs. Equities, bonds, and real estate are natively issued on-chain. The stock market as we know it (T+2 settlement) becomes obsolete, replaced by T+0 atomic settlement networks.

9.2 The “Death” of the Non-Yielding Stablecoin

By 2028, the concept of a non-interest-bearing stablecoin will likely be viewed as archaic. Just as high-yield savings accounts disrupted traditional banking, Tokenized Treasury tokens will force stablecoin issuers to share the yield with users. We expect a convergence where “Payment Stablecoins” (mandated 0% yield by the GENIUS Act) are used strictly for transactional velocity, while 90% of static on-chain liquidity sits in “Investment Stablecoins” like USYC or BUIDL.

9.3 Convergence of TradFi and DeFi

The distinction between “TradFi” and “DeFi” will blur to the point of irrelevance. A user on Uniswap in 2028 will likely be trading a tokenized Apple share against a tokenized Euro-bond, with the trade settling via a bank-issued stablecoin, all pooled in a smart contract. The “front-end” may look like DeFi, but the “back-end” assets will be fully regulated Real-World Assets. This is the endgame: the entire financial system, rebuilt on the internet’s rails.

Table 9.1: Projected Asset Class Growth (2025-2030)

| Asset Class | 2025 Market Size | 2030 Projection (Base Case) | Key Driver |

|---|---|---|---|

| Tokenized Treasuries | ~$9 Billion | $200 Billion | Corporate Treasury Adoption |

| Stablecoins | ~$225 Billion | $2.8 Trillion | Cross-border Payments & Remittances |

| Tokenized Real Estate | ~$20 Billion | $1.5 Trillion | Fractionalization & Liquidity |

| Private Credit | ~$17 Billion | $500 Billion | Emerging Market Demand |

| Tokenized Equity | <$1 Billion | $3 Trillion | 24/7 Trading & Global Access |

10. Conclusion

The transformation of the cryptocurrency market in January 2026 is profound. What was once a speculative casino has matured into the operating system for global financial markets. The GENIUS Act provided the rules of engagement, BlackRock and Circle provided the liquidity, and protocols like MANTRA, Ondo, and Propy are building the highways.

For investors and market participants, the RWA narrative is no longer a “trend” to watch—it is the foundational reality of the modern digital economy. The winners of this era will be those who understand how to navigate the complex interplay between rigid regulatory frameworks and the fluid, permissionless innovation of DeFi. The convergence is complete; the deployment phase has begun.

Sources Used in the Report

- Tokenized US Treasury Products Surge 50x to $7 Billion Market Cap … – mexc.co

- How BlackRock just lost control of the $10B tokenized Treasury … – cryptoslate.com

- BlackRock’s BUIDL Fund Hits $100M Dividend Milestone – Binance – binance.com

- Digital Money – Treasury.gov – home.treasury.gov

- BUIDL Soars with $100M in Dividends and Billions in Tokenized … – coinlaw.io

- In-Depth Analysis of BlackRock’s BUIDL Fund and Its Impact on the … – binance.com

- CoinGecko 2025 RWA Report – assets.coingecko.com

- Fact Sheet: President Donald J. Trump Signs GENIUS Act into Law – whitehouse.gov

- GENIUS Act Implementation – Federal Register – federalregister.gov

- The GENIUS Act of 2025 Stablecoin Legislation Adopted in the US – lw.com

- GENIUS Act Stablecoin Bill Signed into Law: A Breakdown – uk.practicallaw.thomsonreuters.com

- Genius Act: the new era of regulated stablecoins – Regular – regular.eu

- USDY: Tokenized US Treasury Bills Are Coming to Sei – blog.sei.io

- ONDO Finance And The RWA Revolution: How Tokenized Assets … – blog.mexc.com

- Propy Announces a $100M Agentic M&A Expansion to Bring … – ffnews.com

- Latest Propy News – (PRO) Future Outlook, Trends & Market Insights – coinmarketcap.com

- Top Real Estate Tokenization Platforms in 2025 and 2026 – Zoniqx – zoniqx.com

- RWA Outlook 2025: Asset Tokenization Market to Reach $3.5-10T … – binaryx.com

- CityDAO representation of itself as a network city – ResearchGate – researchgate.net

- CityDAO: Pioneering the blockchain metropolis of the future – paragraph.com

- Launch a RWA Platform Like Centrifuge in 2025 – blockchainappfactory.com

- Hamilton Lane, Republic Team on Tokenized Funds for Investors – connectmoney.com

- KAIO Tokenizes HL Private Credit on Sei – Hamilton Lane – hamiltonlane.com

- MANTRA Leads RWA Token Projects with $6.92B Market Cap in 2025 – binance.com

- MANTRA, OM, and RWA: Unlocking the $16 Trillion Real-World … – okx.com

- Mapping the Future of Real-World Assets: The Top RWA … – INX – inx.co

- RWA Tops Crypto Narratives In 2025: CoinGecko Reports 185 … – tradingview.com

- Next-gen markets: The rise and reality of tokenization – Broadridge – broadridge.com

- Top 10 Use Cases of Asset Tokenization in 2025: What’s Real … – zoniqx.com

- How Algorand helped Lofty transform the real estate industry … – algorand.co